Why We’re Investing In Biochar

Our goal is to become the most trusted source of high-integrity, finance-ready carbon outcomes, setting the standard for transparency, verification, and durable climate impact worldwide.

A clear path to real yield.

We invest in things that solve real problems and have a clear path to real yield.

Clear Yield Biochar checks both boxes because it isn’t “a biochar company.” It’s an integrated facility built to turn messy, expensive, regulated waste streams into products (and carbon value) the market already wants.

This opportunity exists because the pain is real and getting more expensive. Fertilizer runoff keeps driving algae blooms and dead zones, and the pressure to change only increases. Wood waste stockpiles don’t just sit there, they create fire risk and release methane as they break down. Animal waste at scale brings nutrient overload, odor, runoff, and rising compliance costs.

This isn’t a “nice-to-have” sustainability story. It’s compliance and economics colliding.

What makes Clear Yield work is the system. Under one roof, the model sequesters carbon through permitted wood waste burial, converts wood waste into biochar, and blends biochar with animal waste to produce eco-fertilizer. That integration is the moat: multiple revenue lanes, more control over inputs, and a clear path to scale. And yield.

See what we did there? ;)

Biochar is the performance ingredient here. It helps stabilize nutrients, reduce leaching and runoff, and improve soil water retention and structure

So it’s not just selling “green,” it’s selling better outcomes.

Location matters too. Central Ohio logistics provide real leverage: efficient inbound access to feedstocks and a strong outbound distribution footprint across a huge chunk of the U.S.

And this isn’t built on hope.

There’s a real operating plan behind it, measurable carbon impact through avoided methane and durable carbon storage, and meaningful Ohio job creation with a project structure that can replicate into additional hubs over time.

If you’re a buyer, feedstock partner, strategic operator, or an investor interested in learning more, let’s talk. Hit us up at theteam@clearyieldbiochar.com.

Why We Invested in a Racehorse

Please meet “Per My Last Email”

Please meet “Per My Last Email” while he works on his “flying lead change” skills.

As a team focused on alternative investments, we’re always on the lookout for opportunities most people never see. Not because they’re “sexy,” but because they’re often inefficient, misunderstood, and mispriced.

That mindset is baked into Partners + Capital. Our 2025 annual letter wasn’t subtle about it: we prefer cash flow over charisma and structure over stories. And we’re obsessive about downside protection whenever the structure allows for it.

So… why a racehorse?

Because racehorse ownership, done correctly, is one of those rare “niche” corners of the market where (1) access is limited, (2) underwriting is inconsistent, and (3) experience + economics can overlap in a way that’s genuinely compelling. And as a boutique firm, part of our job is creating access for friends and family who want alternatives but don’t have the time (or desire) to source and evaluate the weird stuff.

We don’t fall in love with categories. We fall in love with edges.

Over time, our portfolio evolves, but our framework doesn’t. We look for repeatable edges:

knowing how to source

knowing how to underwrite

knowing how to structure

knowing how to protect downside

knowing how to say “no” quickly

That framework works whether we’re evaluating private credit, real estate, oil & gas or something as nontraditional as a Thoroughbred.

Because in alternatives, the best outcomes aren’t “discovered.” They’re designed.

Racehorse investing is niche… and that’s the point.

Most people never invest in a racehorse for the same reasons they never invest in private credit or mineral rights:

they don’t have the network

they don’t know what questions to ask

they don’t have a trusted operator

they assume it’s either for billionaires or gamblers

That gap creates opportunity.

Racehorse ownership is often poorly accessed and poorly underwritten, which is exactly why it can become interesting for the right buyer with the right process.

We can find dealflow for almost any objective

One advantage of living in alternatives is pattern recognition. Investors typically want some combination of:

income

growth

tax strategy

diversification

non-correlated experiences (yes, experiences matter more than people admit)

Our job is to match the objective to the right structure, not force every investor into the same box.

Racehorse ownership can fit different objectives depending on the specific horse, the plan (racing vs. breeding vs. resale), and the structure (direct ownership vs. syndication vs. managed interest). It’s not a one-size-fits-all asset, so we don’t treat it like one.

The underwriting is real (even if the stories are loud)

Horse racing has plenty of hype. We ignore that.

Our lens is closer to how we look at any operator-driven asset:

Who’s running the program? (trainer + management)

What’s the plan? (timeline, race placement, development path)

What are the controllables vs. variables?

What does “downside protection” look like here? (insurance, budgeting discipline, governance, realistic reserves)

What’s the decision-making process when things go sideways?

Because risk doesn’t disappear. It just changes costumes.

And with horses, the variables are obvious: performance volatility, injury risk, illness, liquidity constraints, and a wide distribution of outcomes. That’s exactly why structure and expectations matter so much.

It’s also an “ownership experience,” not just an allocation

Some investments are purely financial.

Racehorse ownership can be financial and experiential: a real asset, in a real ecosystem, with real people, real barns, real race days, and real stories you don’t have to pretend are interesting.

That matters, especially for investors who already have “the usual” exposures and want something memorable that still has an underwriting backbone.

The tax angle: the “hobby loss rule” (and why it’s not magic)

One unique feature of horse-related activities is how they interact with the IRS “hobby loss” framework (IRC §183), which limits deductions if an activity is not engaged in for profit.

Here’s the relevant nuance:

The IRS generally presumes an activity is for-profit if it shows a profit in at least 3 of the last 5 tax years.

For activities that consist primarily of breeding, showing, training, or racing horses, that safe-harbor window extends to 2 of the last 7 tax years.

That said, two important caveats:

This is a presumption, not a loophole. The IRS can challenge it based on facts and circumstances.

If you don’t meet the safe harbor, it doesn’t automatically become a hobby. It just means the analysis becomes more fact-specific (businesslike operations, recordkeeping, expertise, time/effort, profit intent, etc.).

So yes, horse activities have a unique wrinkle inside the hobby loss framework. But the real takeaway is simpler:

If you’re going to do this, do it like a business. (And talk to your CPA before you do anything aggressive.)

Why we said “yes” to this niche category

We didn’t invest in a racehorse because we wanted to be interesting.

We invested because it fit our philosophy:

a niche market with access constraints

underwriting inconsistency (which creates pricing inefficiency)

the ability to structure participation thoughtfully

and a compelling ownership experience layered on top

In other words: not hype, not narratives, not “maybe someday” math.

If you’re curious how we think about niche alternatives (racehorses included) we’re always happy to walk through the framework, the risks, and what “good structure” actually looks like.

2025 Year In Review

To our Partners + Capital Investors, Friends, and Supporters,

Each year, we write an annual letter to capture what we researched, what we’ve learned, and what we’re carrying forward across markets, across deals, and across the messy human part of building anything meaningful.

Partners + Capital was built (nearly ten years ago) on a simple idea: seek real assets, real cash flow, and real underwriting then do it with discipline.

Not hype. Not narratives. Not “maybe someday” math.

And yes, results matter.

In 2025, our focus on disciplined alternative investing delivered strong performance for many of our LPs and Investment Partners, while staying grounded in what we care about most: principal protection and predictable monthly returns whenever the structure allows for it. (As always: markets change, and past performance is not a promise.)

What 2025 reinforced

2025 felt like a year where the market stopped pretending.

Cheap money is no longer the default setting. Capital became more selective.

Projects relying on “perfect conditions” got exposed. And the deals that worked best were the ones built on fundamentals:

• Cash flow over charisma

• Structure over stories

• Downside protection over upside fantasies

When you live in alternatives, you learn quickly: the goal isn’t to be the loudest in the room. It’s to be the last one standing.

The throughline: first principles and repeatable edges

Over time, our portfolio has evolved, but our mindset hasn’t.

We don’t fall in love with categories. We fall in love with repeatable edges:

• knowing how to source

• knowing how to underwrite

• knowing how to structure

• knowing how to protect downside

• knowing when to say “no” quickly

It’s why our core focus continues to be the three categories that built this firm:

1) Private Credit: boring, beautiful, and back in fashion

Private credit remains one of the cleanest ways to align incentives: define the risk, price it appropriately, secure it when possible, and get paid for being early and decisive when banks can’t (or won’t) move.

Our job is not to “chase yield.” Our job is to create intelligent certainty with clear covenants, clear collateral, and clear repayment expectations.

2) Real Estate: reality won

Real estate in 2025 demanded realism. Operating costs stayed stubborn. Insurance didn’t magically get cheaper.

Construction still required humility. And the winners weren’t the best PowerPoints. They were the best operators.

We continue to prioritize projects with:

• durable demand

• thoughtful basis

• realistic rent assumptions

• clear execution paths

• and sponsors who have actually done the work before

3) Oil & Gas: misunderstood, cash-flowing, and still essential

In the world of soundbites, energy investing is often discussed like a moral debate instead of an economic one.

We prefer ground truth.

Energy demand is real. Production matters. And well-structured oil & gas opportunities can offer what many portfolios are missing: cash flow, tax advantages (where applicable), and diversification that doesn’t depend on Wall Street’s mood.

What we learned (again)

1) Great deals are designed, not discovered.

The best outcomes come from structure. Alignment, protections, clarity, and incentives that don’t collapse under pressure.

2) Risk doesn’t disappear. It just changes costumes.

In a hype cycle, risk looks like optimism. In a downturn, risk looks like panic. Our edge is staying rational in both.

3) Your calendar predicts your outcomes.

The strongest operators we know are obsessive about priorities, execution, and follow-through. Not motivation. Systems.

Looking ahead to 2026

We’re heading into 2026 with confidence along with a healthy level of skepticism.

We plan to stay disciplined in our core categories (private credit, real estate, oil & gas) while selectively expanding into a few alternative areas where we believe the market is inefficient and the ownership experience is compelling.

Art & collectibles, race horse ownership, and other niche categories that are often poorly underwritten and poorly accessed.

But let me be very clear:

We are not expanding to be “interesting.”

We are expanding only where we believe we can be excellent; with the same underwriting mindset and the same respect for downside.

A note to builders and operators

If you’re building a company, a project, or a portfolio in this environment: craftsmanship matters again.

• Build things people actually want.

• Keep standards high.

• Protect your balance sheet like it’s fucking oxygen.

• Be rational and ruthless with capital allocation.

• Don’t confuse “busy” with “effective.”

This is a Darwinian business. You either improve with the moment or the moment improves without you.

Thank you.

We don’t take your trust lightly. Not once. Not ever.

Thank you for letting Partners + Capital be part of your financial story. As a boutique firm focused on alternatives, we’re definitely the black sheep in the industry.

However, we are grateful for the confidence you’ve placed in us and we’re excited about what we’re building next.

If you’d like to review year-end planning items, portfolio updates, or discuss where you want your alternatives exposure to be in 2026, please reach out. We’re always happy to help.

With gratitude,

David Hunegnaw

Partners + Capital

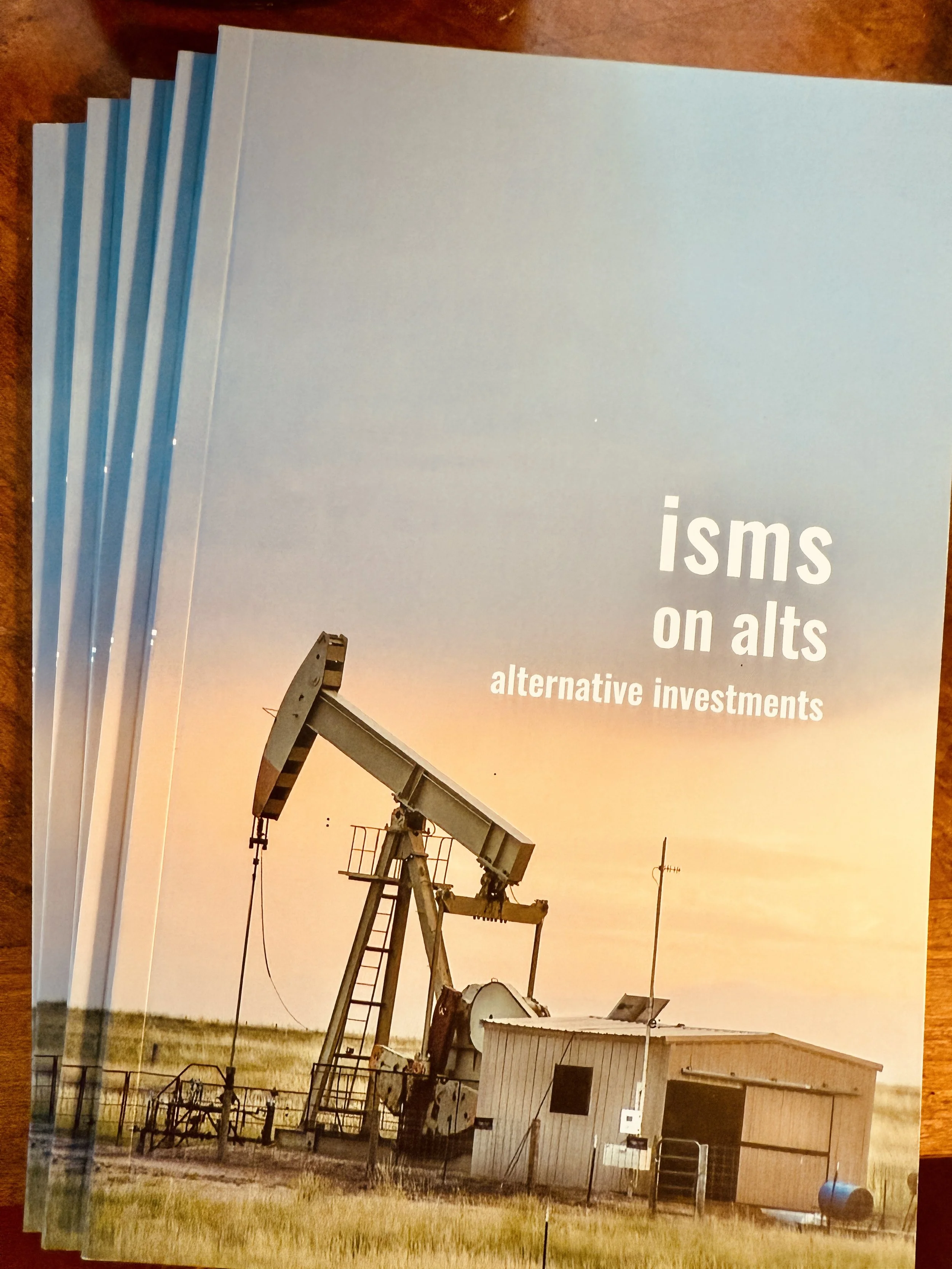

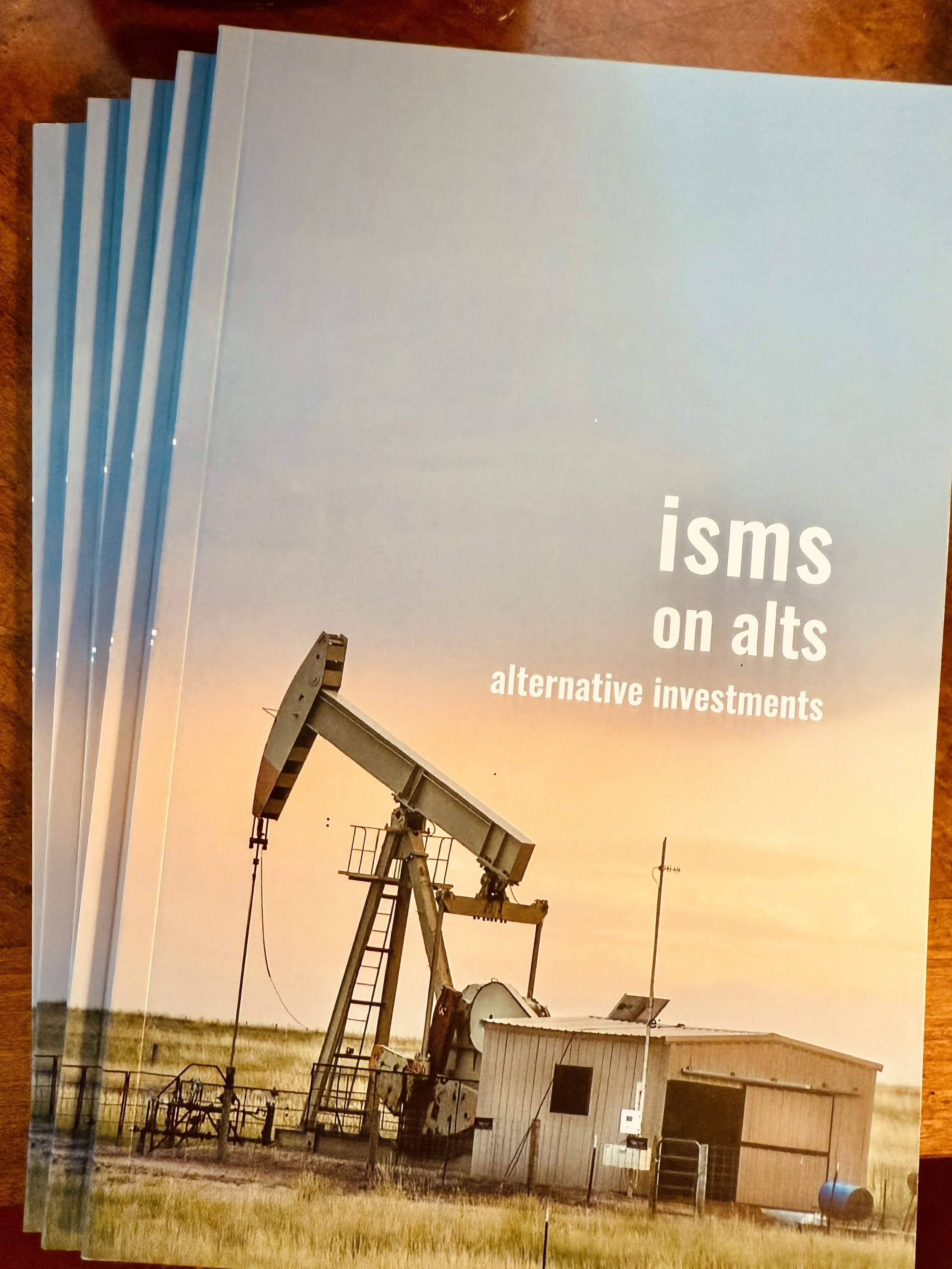

Why We Wrote ISMs on Alts

This book isn’t for the ultra-wealthy or high-net-worth (HNW) investor. HNWs already know these “isms.”

This little book is for the almost-there investor. Let’s call them the medium-net-worth (MNW) investor.

Smart. Capable. Disciplined. Yet locked out.

Not quite high-net-worth. Yet too much momentum to settle for average.

MNW individuals don’t need another guru. They don’t need another stock tip. They need a new lens. And a new language.

An alternative language.

ISMS on Alternative Investments

Why We wrote ISMs on Alts (Alternative Investments)

At Partners + Capital, we spend our days in real assets and alternative categories, where the details matter and incentives matter even more.

And “storytime” is not a strategy.

We wanted a way to share what we’ve learned without turning it into a lecture.

So we wrote it the way we think: short, direct, and occasionally a little spicy.

What you’ll get out of it

You’ll find ISMs that touch on:

how to think about risk (without pretending it doesn’t exist)

why liquidity is a feature and a warning label

how to spot great structure vs. great marketing

why “exclusive” doesn’t always mean “good”

If you’ve ever felt like alts are either too opaque or too hyped, this is for you.

The point

ISMs on Alts isn’t meant to replace diligence. It’s meant to sharpen it.

And if one line sticks in your head long enough to help you ask a better question before you invest?

Mission accomplished.

If you’d like a copy of the book, use this link for our eBook or email me for a print version.

Want to talk about where alts fit in your plan? Just let me know.

Why We Invested in Private Credit

Private Credit wasn’t a “trend” when we first leaned in. It was simply the cleanest answer we could find to a question we kept asking:

Private Credit wasn’t a “trend” when we first leaned in. It was simply the cleanest answer we could find to a question we kept asking:

How do you generate real yield with real downside discipline without needing perfect market timing?

Nearly ten years ago, we made the decision to commit to Private Credit. Not because it was fashionable. Because it was logical.

We did it years ago. Before most people were talking about it

When we entered Private Credit, the asset class was still “insider baseball” for most investors. Today, everyone has a Private Credit opinion. Back then, it was mostly institutions and specialists quietly doing the work.

We liked that.

Private Credit offered something we value deeply: return potential you can underwrite rather than hope for. We weren’t betting on a multiple expansion story. We were underwriting cash flow, collateral, structure, and repayment.

We waited until we had a real due diligence engine

We didn’t start Private Credit because we wanted to. We started because we were ready to.

Private Credit is not passive. It rewards operators, not tourists.

So we built the muscle first:

A robust due diligence team

A repeatable underwriting standards

Legal/structuring horsepower

Monitoring system (because what matters isn’t what you underwrite, it’s what you track)

In private credit, the work isn’t optional. It’s the product.

We identified a strategy designed to reduce default rates

A lot of lenders chase yield, then “manage” risk later.

We do it the other way around: we design for repayment first, and let yield be the reward for discipline.

The core of our approach is simple:

We believe structure creates behavior. Covenants, reporting requirements, and incentives matter.

We prefer clarity over creativity. If the repayment path isn’t obvious, we pass.

We underwrite the downside like it’s the only side. Because in credit, it is.

And we obsess over the things that quietly reduce defaults:

Borrowers with predictable demand (not “hype cycles”)

Strong unit economics and cash conversion

Conservative leverage

Multiple ways to get repaid (cash flow, collateral, guarantees, contractual revenue, etc.)

Early-warning monitoring so we’re not surprised

The goal isn’t just fewer defaults. It’s fewer losses. Because structure, collateral, and proactive oversight change outcomes even when things get choppy.

Why Private Credit still fits our DNA

We’ve always been a firm that values:

control

craft

repeatability

risk-adjusted outcomes

Private Credit checks those boxes. It’s an arena where process beats prediction. And where discipline compounds.

Eight years in, our thesis hasn’t changed:

Private Credit is what happens when you want return. But you respect risk.

Why We Invested In Pizza

Invested in What Others Overlook.

We’ve built tech companies. We’ve led real estate developments. We’ve pitched investors in boardrooms and elbowed our way through food stalls for deals.

But the move that gets the most raised eyebrows from our investors?

We invested in Sourdough Pizza Bros.

Not just any pizza. Sourdough Pizza Bros. A brand built on ancient fermentation, bold creativity, and a relentless obsession with crust that actually means something.

Now, we know what you might be thinking: pizza? Isn’t the pizza market saturated?

Doesn’t every strip mall already have a “#PapaDough or #DomiNoDough” something?

Sure. But that’s exactly the point.

Pizza Isn’t a Trend. It’s a Behavior.

Let’s start with the numbers:

460 slices of pizza are consumed every second. Every second!

1 in 8 Americans eat pizza on any given day.

94% of Americans eat pizza regularly.

The average American eats 46 slices per year.

Americans eat a third of all pizza consumed worldwide.

About a third of all consumers consider pizza a valid breakfast.

Let that first one sink in: 460 slices per second?

That’s not a fad — that’s infrastructure. Pizza is embedded in our culture, rituals, and lives.

So when we identified the opportunity to invest in a company that wasn’t just another chain… but rather a brand built on fermentation, flavor, and soul… we knew it was worth betting on.

What Makes Sourdough Pizza Bros Different?

We’re not trying to be your 2AM, soak-up-the-suds pizza. We’re not built on gimmicks, fake crusts, or factory shortcuts.

Our dough is aged for 36 hours and backed by a 100-year-old starter.

It’s stretched by hand.

It’s never put into a machine.

It’s built to rise.

Every slice we serve is a conversation between the past and the future — where ancient fermentation techniques meet modern flavors, bold sauces, and a swirl of personality you won’t find in a franchise playbook.

We call it “Crust with a Past. Pizza with a Future.”

And it’s not just about ingredients. It’s about brand.

Voice.

Humor.

Ownership.

Culture.

We’re a company with something to say and the taste to back it up.

So Why Us? Why Now?

Because we don’t just invest in markets. We invest in meaningful and measurable moments, and we are solely focused on serving future entrepreneurs in underserved and overlooked markets.

We invest in things people talk about when they leave the table.

We invest in underdogs with unfair advantages.

We invest in products with ritual built in.

We invest in things that scale not just across ZIP codes — but across identity, story, and community.

Sourdough Pizza Bros isn’t just a pizza brand. It’s a rebellion against the soulless, the soggy, and the same-old.

We exist…

- to serve.

- to prove that a product can be personal.

- to be a startup experimenting how we can support the overlooked and the underserved.

In an era where everyone’s trying to be the next big tech thing, we decided to be something else:

Fresher. Healthier. And built to last.

Why We Created Garden Park on High

Why we created Garden Park on High.

Why We Created Garden Park on High

At the heart of the Short North, something new is growing.

Columbus has long been defined by its ability to evolve—quietly, purposefully, and with grit. We’ve watched the Short North become a canvas for artists, a haven for small businesses, and a community full of contrast and color. But we’ve also watched something else: the growing tension between what this neighborhood was built on and what it's becoming.

Garden Park on High is our answer to that tension.

We didn’t just want to build another high-rise. We wanted to plant something.

Rooted in Respect for Place

Garden Park sits at the northern edge of the Short North, a place we call the “North Short North.” It’s a neighborhood with deep layers—industrial bones, artistic flair, immigrant families, and entrepreneurial energy. It’s where historic churches meet modern coffee shops, and where alleyways still carry echoes of old Columbus.

Too often, development forgets its surroundings. Garden Park is a project shaped by the neighborhood—not imposed on it. From day one, we prioritized community voices, cultural texture, and architectural respect. We wanted to build something that didn’t just rise above the community—but that belonged to it.

A Garden for All

The name isn’t just a metaphor. We envisioned a place where affordability, accessibility, and aspiration could coexist. A place where a schoolteacher, a software engineer, and an artist could all call the same building “home.”

That’s why Garden Park includes:

Affordable Housing on the lower floors—because everyone deserves access to the heart of the city.

Mid-market Rentals for working professionals and young families who want to grow with the neighborhood.

For-sale Condos at the top—for those planting longer-term roots.

Public Spaces filled with greenery, art, and a sense of calm amid the city’s buzz.

More Than Just Units and Elevators

We believe buildings should do more than cast shadows—they should cast vision. Garden Park is designed not just to house people, but to elevate them. Through partnerships with local nonprofits, small businesses, and civic leaders, we’re weaving this project into the social and economic fabric of Columbus.

We’re also proud to bring local entrepreneurship into the fold—from Black-owned coffee shops to women-led design firms—so the project reflects the people and creativity that make this city remarkable.

A Future That Doesn’t Forget

Ultimately, Garden Park on High is about making sure that as Columbus grows, it doesn’t forget the people who built it, the artists who painted it, or the families who shaped it. We believe development can be both ambitious and inclusive. Garden Park is our proof of concept.

And like any good garden, it’s only just beginning to grow.

Why We Invested In Marine Field

100 Well Legacy + 40 Year Track Record = Right Oil Play

100 Well Legacy + 40 Year Track Record = The Right Oil Play

At Partners and Capital, we don’t chase hype, we pursue long-term value. That’s why our investment in Marine Field, located in the Southern Illinois Basin, wasn’t just another oil and gas deal. It was a calculated move into a proven asset with operational predictability, decades of production history, and meaningful upside.

Here’s why we chose to invest.

1. Proven Reserves in a Known Basin

Marine Field isn’t speculative. It’s a legacy asset with over 40 years of continuous production in a basin that’s known for steady output and strong geologic fundamentals. With more than 100 wells already drilled, the field’s performance has provided a reliable data set for future development and enhancement.

We’re not guessing here, we’re building on decades of verified productivity.

2. Cash-Flow Generating From Day One

This isn’t a bet on a future discovery. Marine Field is already producing. Our capital isn’t tied up waiting for a miracle well, it’s being deployed into operations that are generating immediate returns. That’s a rare feature in today’s capital-intensive energy environment.

3. Low Lifting Costs, High Margin Potential

Thanks to the shallow depths of the Southern Illinois Basin and the mature infrastructure surrounding the project, Marine Field benefits from unusually low lifting costs. That translates to margin resilience, even in commodity cycles where prices soften.

We like assets that protect the downside while allowing for considerable upside. Marine Field does both.

4. Scalable Opportunity With Room to Optimize

The field isn’t tapped out… it’s under-optimized. New well reworks, modern completion techniques, and enhanced recovery strategies can unlock additional reserves at relatively low cost. With over 100 existing well sites and expansion potential, this isn’t just a yield play. It’s a growth story.

5. Aligned Operators With Skin in the Game

We don’t invest in deals, we invest in people. Erinie, Darshan and the Marine Field team has deep operational roots in the region, and their interests are aligned with ours. They’ve committed capital alongside ours, and they’re not incentivized by hype, they’re incentivized by performance.

Final Thought: Back to Basics, Forward with Focus

In a time when capital often chases the flashiest headlines, Marine Field reminds us that smart investing is about fundamentals, strong geology, predictable cash flow, and trusted partners.

At Partners and Capital, we’re proud and excitede to be part of this next chapter in the Marine Field story.

It’s not just oil.

It’s opportunity, refined.

Why We Invested in Cantera Negra

We don't chase trends. We follow conviction.

At Partners & Capital, we don't chase trends, we follow conviction.

So when the tequila wave started to crest, we didn’t run to the nearest celebrity-backed bottle or glittery brand with slick packaging. We took a different route. We went looking for depth, for legacy, for craft. And that path led us to Cantera Negra.

A Spirit with Soul

Cantera Negra doesn’t scream for attention. It doesn’t need to. Each bottle carries over four decades of artisanal tequila-making, crafted by a family that’s been quietly perfecting their process in the hills of Jalisco long before “premium tequila” became a marketing gimmick.

This wasn’t a celebrity vanity project. It was a masterclass in doing things the hard way. The right way.

That’s our kind of story.

Premium Product. No Pretense.

In an era when most brands are chasing exits, Cantera Negra is building a foundation.

Our tequilas, from the silky smooth Silver to the bold, barrel-aged Extra Añejo are made with 100% blue agave, aged beyond industry standards, and blended for balance, not hype. The taste is undeniable, and the growth is organic, driven by real fans, not influencers.

That’s a rare thing in this market.

The Market Is Loud. We Listen Differently.

We don’t believe in being the loudest. We believe in spotting signals through the noise. Cantera Negra had all the right ones:

Best-in-class product backed by years of refinement

Authentic brand story rooted in heritage, not hype

Smart expansion strategy that favors quality over velocity

Founders we trust, who understand the value of patience and precision

In a saturated space, that kind of intentionality wins.

Long-Term Glasses Only

We didn’t invest in Cantera Negra because we think tequila is hot right now. We invested because we believe it will still be relevant (and respected) ten years from now.

This is a brand with legs. And not just the kind that run down a glass.

At Partners & Capital, our capital follows culture, taste, and truth. Cantera Negra checked all three.

—

Partners & Capital is a boutique alternative investment firm focused on consumer, real estate, and overlooked opportunities others miss.